Wait! Before You Go…

Stay connected and get the latest insights in contract management!

Visit our LinkedIn Page to join a community of professionals and stay updated on industry trends, best practices, and expert tips from Contractmanagement.online.

![]()

The term ‘Sustainable Supply Chains’ mean different things to different people. Not only by customers and suppliers in your region, but those in other regions that have different priorities and investment criteria concerning sustainability.

To help organisations talk from the same perspective, there have been quite a few (and confusing) attempts to standardise reporting by businesses of their climate change actions. But from June 2023, the Reuters Events report Sustainability Reporting Enters the New Era of Standardisation, notes there will be just a small set of official reporting standards – UN, EU and US, together with a new set of acronyms for a Supply Chain professional to know.

UN: the International Sustainability Standards Board (ISSB) standards are due for publication in June 2023. To be effective in a country, they will require adoption by that national jurisdictions. Countries can amend the standards and develop their own rules for enforcement under national legislation.

EU: the European Sustainability Reporting Standards (ESRS) are due to be published by the European Commission in June 2023. The ESRS are based on the Corporate Sustainability Reporting Directive (CSRD) legislation, which is the mandate for the standards and came into force in January 2023. About 6,000 listed and 40,000+ private companies (SMEs are later) will come within the scope of the standards. The companies are required to report on their global supply chains. Non-EU businesses with operations in the EU will also be included, so in both instances, all suppliers that have items used in ‘European’ products will eventually need to comply with the standards. The first reports under these standards are due in 2025

USA: The Securities and Exchange Commission (SEC) is due to publish rules on climate risk disclosure in Q2 2023. This will affect reporting about sustainability for about 12,000 U.S. listed companies. The first reports under these rules are due in 2025

The European ESRS standards are broader than either the ISSB or SEC requirements. The ESRS has reporting of policies and outcome targets, with an emphasis on businesses reporting the actions taken.

Materiality is the term used to evaluate the impact that a business risk could have on a company and possibly its shareholders and therefore whether it should be included in corporate reporting. The CSRD has broadened the concept to cover company risks and their impact, which is called ‘Double Materiality’. This means that companies must consider how vulnerable they are to the effects of climate change, plus how the company’s activities impact people and the environment. The ISSB standards do not incorporate the concept.

The Global Reporting Initiative (GRI) did not merge with the ISSB. However, the GRI will likely remain as a popular methodology used by companies for sustainability reporting. Outside of the US, companies may use the ISSB or ESRS standards for financial material reporting and the GRI for what is called materiality (or impact) reporting. The GRI incorporates a guide to using materiality assessments.

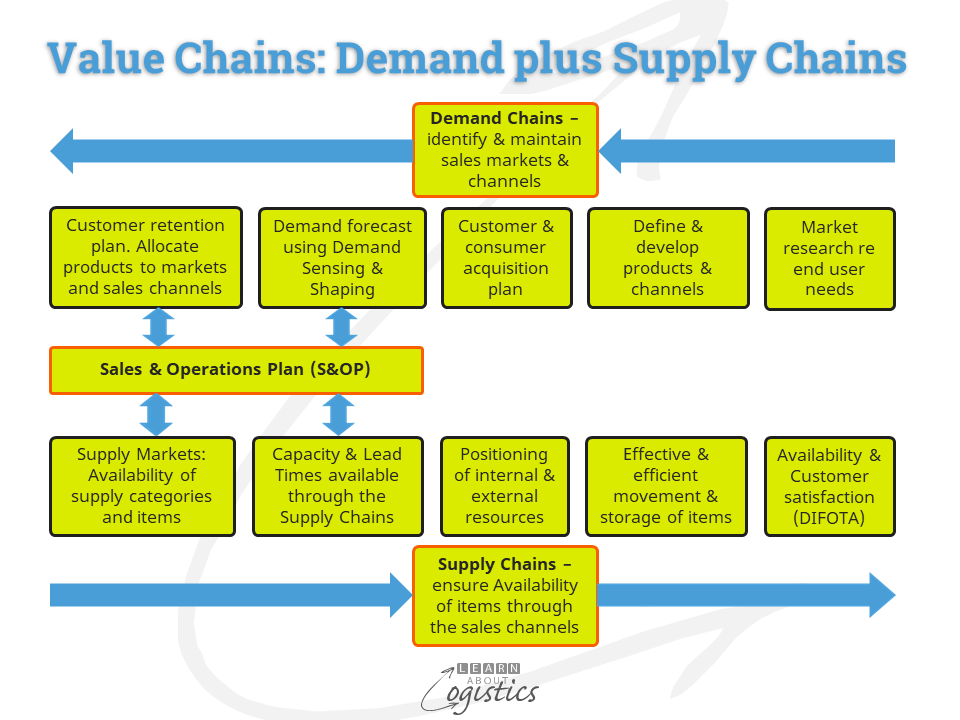

Both the ISSB and ESRS standards require reporting about what they call the ‘value chain’ of a business. They use the same expressions – “the full range of activities” and “all relationships”. The standards note that ‘value chain’ is both upstream and downstream of a business and is not restricted to ‘supply chains’ or direct (Tier 1) suppliers. The diagram illustrates the LAL definition.

The ESRS standards also refer to the concept of due diligence; that is a company identifying, managing and mitigating risks in its value chains. These include Environment (through Scope 1, 2 and 3 reporting) and Social reporting. Social includes:

Governance addresses business conduct. The ESRS standards include corporate culture, fair relationships with suppliers, anti-corruption processes and transparent political influence and lobbying.

An important criterion for planning reductions in Environment is time. At current levels of global emissions, the remaining global ‘carbon budget’ will be used by 2033. This requires your supply chains to be in a position of ‘net zero’ emissions by 2030.

An MIT survey State of Supply Chain Sustainability 2022 noted that the ‘base camp’ Supply Chain practices required to manage sustainability were: Supply Chains Network Mapping to understand the potential risks in your supply chains; Supplier Audit and a Code of Conduct for both the company and for Tier 1 suppliers. Only when these are in place can the Supply Chains group move to the next level: Implementing standards for action and reporting; linking IT systems for co-operation with Tier 1 suppliers and developing collaboration with Tier 1 suppliers. Depending on the resources deployed and time allocated, completion of these two stages can take up to three years, but is this too long?

The MIT survey also noted that Supply Chains Sustainability (SCS) “is not a zero-sum game between environment and social, both can be pursued. However, your Supply Chains group must be able to adapt their sustainability efforts to the prevailing context. Customers can change their expectations and dimensions of sustainability, especially across different regions”.

Our planet is tracking for a temperature rise of between 2.4C and 2.6C. The outcome will be a catastrophic impact on human life and the ecology. Many (most) businesses around the world know the future is not good, but profits come first, so leave it to future generations to fix the problem. The new standards attempt to correct this approach, but they are not ‘best practice’ in Sustainability. That is up to you and your colleagues to achieve.

Author: Roger Aokden

Procurement sits at the forefront of an organization’s social and sustainability efforts. This is because organizations are now judged not only on their internal practices, but also on their ability to enforce ESG...

Regulators around the world are sending a consistent message to companies that operate or source internationally, which is that they must take ownership of their supply chains. In addition, multinational companies...

Contract management in healthcare is a critical, yet often complex, process that directly impacts an organization's operational efficiency and financial health. With the advent of modern technologies, the...